Customer demand, regulatory support and advancing technology are fuelling a boom in fintech in Korea, according to an equity research report by Credit Suisse.

Fintech is part of a broader trend in tech startups and unicorns (startups valued at $1 billion or more), of which there are now eight in Korea, according to the August 29 report, written by lead analyst Park Jeehoon.

Biotech and retail services are the hottest areas winning the most investment. But fintech investment is also thriving, especially in payments, crowdfunding, and virtual banking.

Today there are more than 9 million daily users of mobile banking services in Korea, about double the number from 2013. Even more striking: 90% of banking transactions in Korea are today made online.

Show me the money

This helps explain the ongoing flood of money going into the country’s startup scene.

The Korea Venture Capital Association says startups received W3.4 trillion of investments in 2018 and are on track to receive W4 trillion this year. In the first half of 2019, 826 startups received investment, up 16.3% year on year (there are now over 300 fintech startups in Korea). Funding for startups is also shifting from mainly early stage to also include growth-phase companies.

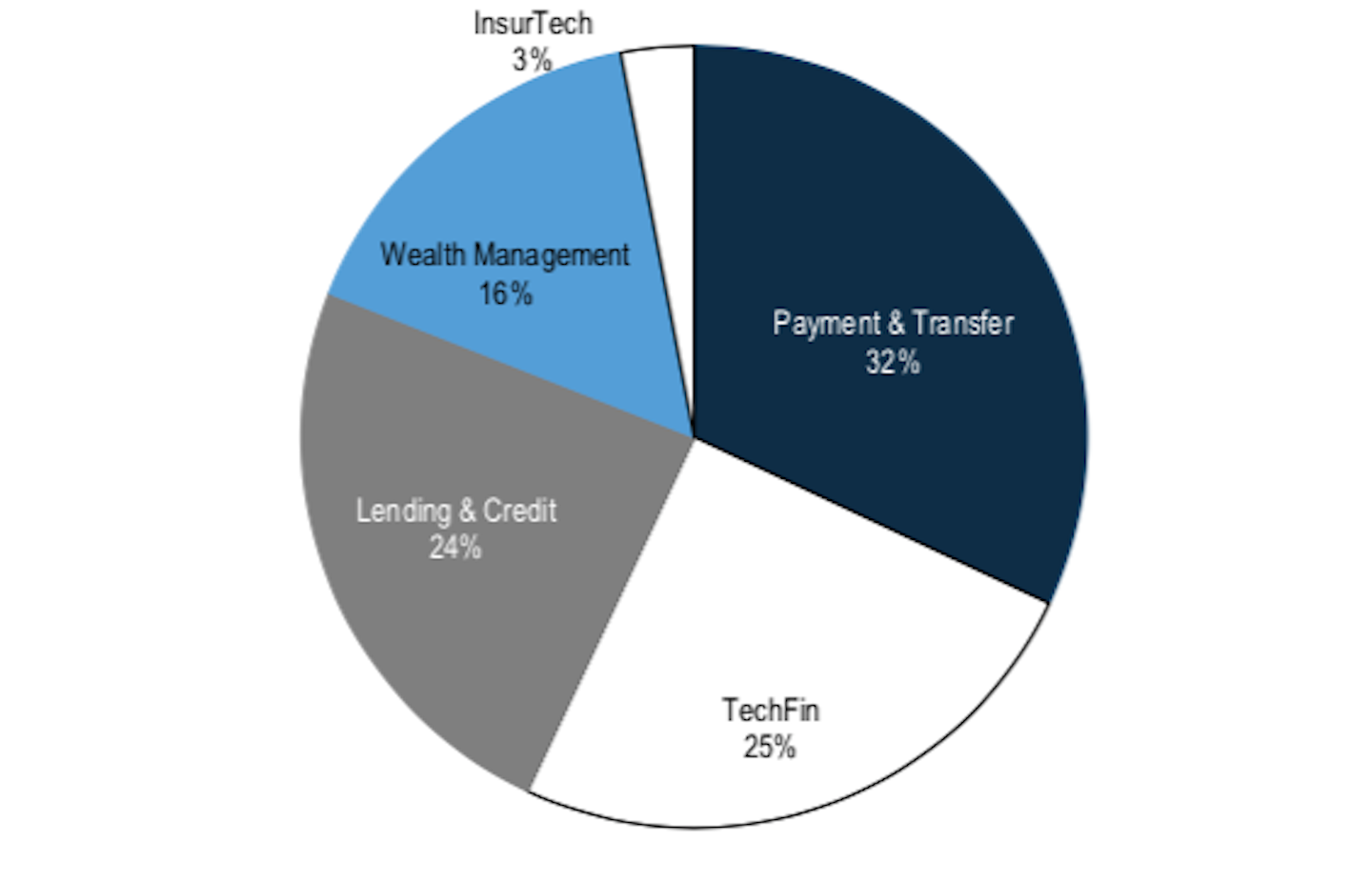

Within fintech, payments and money transfer account for 32% of investment (see chart, main image); ‘techfin’, that is investments from internet companies like Kakao and Naver, is 25%; lending and credit startups are getting 24% of the money; digital wealth 16% and insurtech 3%.

Korea’s fintech leaders

Credit Suisse cites several fintechs as new standardbearers for Korea. The biggest startup in terms of valuation is the unicorn Viva Republica, whose backers include PayPal and Altos Capital. Valued today at W2.7 trillion, the 2013-vintage company operates a popular financial platform app called TOSS.

Others include Wadiz, a crowdfunding platform that provides seeding solutions for startups and new business ventures; and insurtech Bomapp, supported by conglomerate Lotte Group and KB Financial.

The leading banks have also teamed up to jointly fund Honest Fund, a digital wealth and lending platform; its shareholders include KB Investment, Hanwha Investment, and Shinhan Capital, a Who’s Who of Korean private-sector banking.

Just as notable, Korea’s traditional banks are also busy with their own fintech initiatives.

Hana Financial is setting up a globally integrated platform based on blockchain; Shinhan is operating a mobile financial service that combines banking, insurance and wealth management; and Nonghyup Financial is the market leader in open banking, using APIs to connect with affiliates and third-party companies to share customer data (on customer request).

Regulatory support

Oddly, the Credit Suisse report omits analysis of the hugely successful Kakao Bank or its fellow virtual bank, K-Bank (our story on VBs touted Kakao as the most important model for incoming VBs in Hong Kong and Singapore). It does list out the 33 tech investments made by internet parent Kakao into startups, from payments to crypto to gaming and healthcare.

But it does mention that the regulators in Korea are preparing to license a third virtual bank in 2020.

This is just one aspect of how regulators in Seoul have supported fintech, and why it continues to attract new players and financial backing.

The Financial Services Commission has taken steps over the past several years to support innovation. It has eased regulation on how firms authenticate customers, legalized crowdfunding and virtual banking (aka neo-banking), and blessed a blockchain-based authentication platform called BankSign.

This year, in April, the FSC launched a fintech sandbox giving companies a four-year forgiveness period to test new products. This coming month, it will set tougher mandates for open banking, to be followed next year with the debut of “MyData”, requiring open APIs between banks and fintechs to provide new financial services based on customer personal data.