Banking & Payments

How PBoC’s digital RMB might work

Michelle Li, head of research at AMTDi, outlines what we know so far about China’s plans for a digital yuan.

On Aug 10, Mu Changchun, deputy director of the People’s Bank of China’s (PBoC) payment department, confirmed the potential launch of digital RMB, which has been studied for five years. On August 20, the state media People’s Daily also published an article on digital RMB (or “d-RMB”) highlighting its potential in retail payments.

This was not entirely unexpected, especially after Facebook announced its plan for Libra, a sovereign-neutral cryptocurrency.

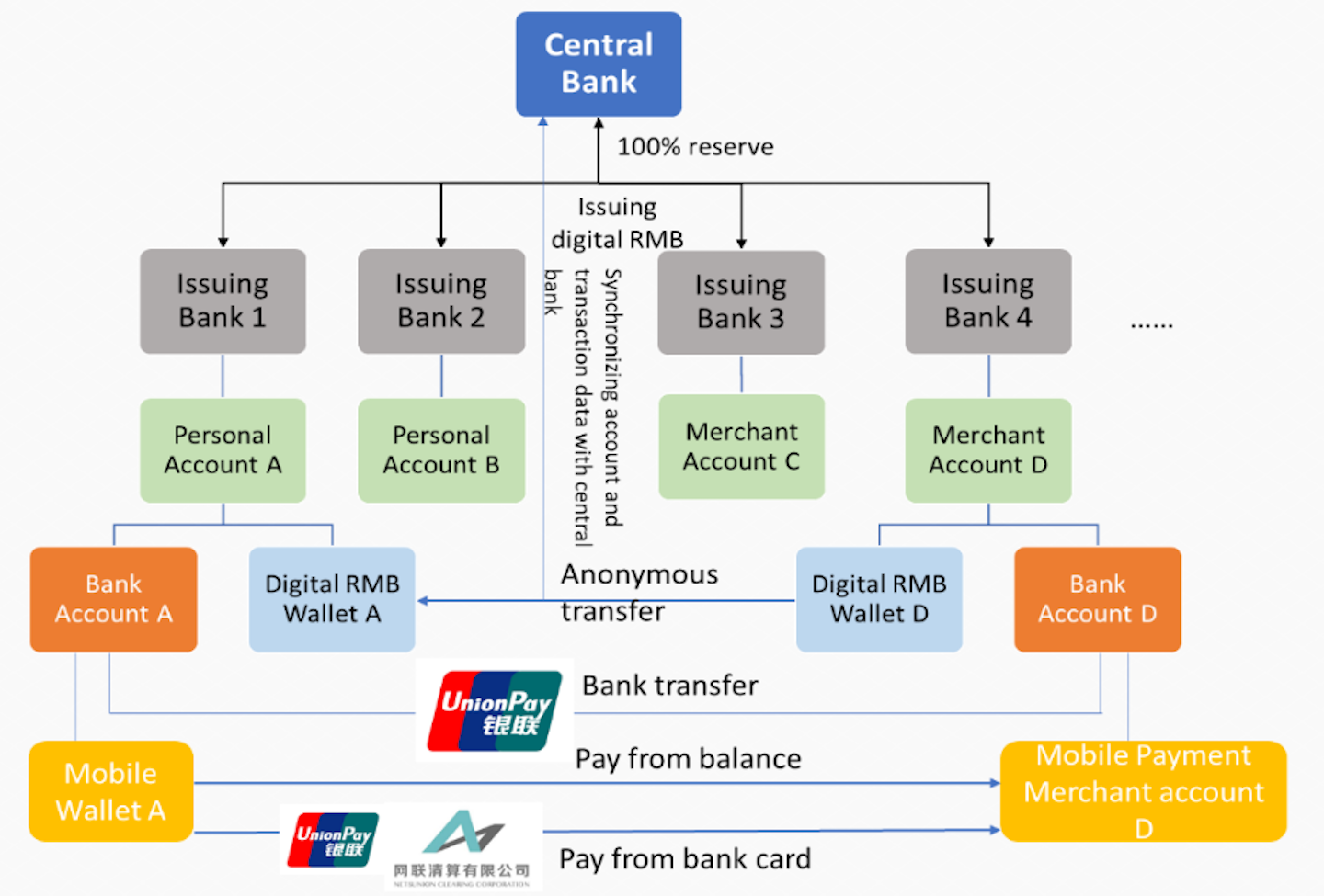

It seems that China’s central bank will stick with a centralized model, unlike the decentralized model taken by most cryptocurrencies. According to Mu, the digital RMB will run on a two-tier operating system: the central bank first converts renminbi balances held by commercial banks or other issuing agencies into d-RMB, and these commercial banks will then issue the digital currency to the public. (UnionPay and NUCC already perform a similar function for bank-issued credit cards.)

In this process, the central bank will adhere to a centralized ledger model. But there will be some leeway around the infrastructure: PBoC will not determine what clearing and settlement technology is adopted by issuing agencies. Mu mentioned that each issuer could have its own technology and system; blockchain will only be one of the options. The issuing agencies need to be institutions with large number of retail bank accounts or wallets; therefore, are likely to be the top SOE banks and mobile-wallet companies.

A cash alternative

D-RMB will retain some of cash’s features of anonymity. At the same time, however, it also can solve counterfeit money problem, and prevent money laundering and the financing of illegal activities, Mu Changchun said. Digitizing the currency will support retail payments and the development of inclusive finance.

Mu also mentioned the d-RMB system can help PBoC adopt a negative interest-rate policy when necessary. On the other hand, Mu thinks that d-RMB cannot add much value in M1/M2 circulation, which are based on bank accounts and are already digitalized.

Digital RMB wallet?

According to Mu Changchun, anonymity of d-RMB can be partially realized as the account can be separated from user’s bank account. A possible alternative to bank accounts could be a digital RMB wallet.

The d-RMB transactions, which may be anonymous between users, are managed by the issuing agencies, with account and transaction information synchronized with the central bank. This would be supplementary to bank transfers and mobile payments, which are cleared and settled through UnionPay, NUCC, or inside the mobile payment companies.

Better transparency

Today, e-wallet balances are estimated to be more than Rmb1 trillion ($140 billion) in China versus Rmb7 trillion ($977 billion) in cash. Mobile payments play a key role in replacing cash and likely have surpassed cash transaction volumes: for example, in the first quarter of 2019, mobile payments reached Rmb84 trillion ($11.7 trillion), according to iResearch.

In the same e-wallet system, if bank accounts are not involved, payments out of wallet balances settle and clear directly in the wallet system without passing through UnionPay or NUCC. This type of transactions falls out of the oversight of PBoC. Digital RMB can be a solution to this problem, by bringing e-wallet balances into central bank’s fold without affecting the money supply.

The introduction of d-RMB wallets may hurt the dominance of Alipay and WeChat Pay. These two companies, thanks to their seamless user experience and network effects, today claim more than 90% of the mobile payments market. But if users can pay directly out of d-RMB wallets, then they wouldn’t need to rely on the servers of these private companies.

This article is courtesy of Michelle Li, head of research at AMTD International in Hong Kong.