The abundance of hard-to-research, inefficient, complex and different investment problems in Asia make this a region where classical, fundamental hedge funds are able to see off the threat of artificial intelligence-driven competitors.

So says a number of hedge fund founders and managers in Hong Kong in response to a new report suggesting that strategies built around machine learning are posing a dire threat to many alternative investment shops.

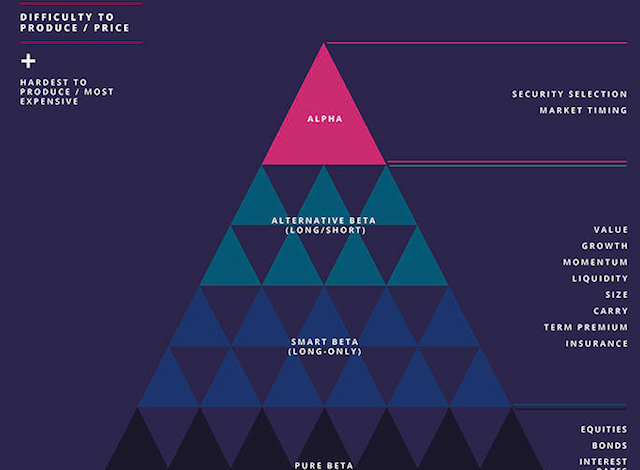

The study, commissioned by London-based Alternative Investment Managers Association (AIMA), says the industry’s shift to low-cost smart beta or alternative beta products is opening it further to competition against machine-led strategies.

Computer-driven products are industrializing hedge funds, making them liquid, cheap, and accessible to larger institutional investors. There remains, at the top of this animal kingdom, a group of classical, research-driven firms that still earn high fees in return (supposedly) for consistent outperformance. How long can the classical hedge funds survive against the AlphaGos and Terminators of this world?

London gloom…

The answer may depend on where you live. For those in New York and London, where data is aplenty, the outlook is stark, and the competition for talent is fierce.

“It’s a fight in the West to win and retain talent against the likes of Google and Facebook,” said Murray Steel, Asia COO at Man Investments. “In London, big tech is still cool.”

Tom Kehoe, London-based global head of research at AIMA, says the tech headwinds in markets such as the UK and US will only get worse for hedge funds. “Today there are 16 trillion gigabytes of data out there,” he said. “In ten years, there will be ten times that amount. What’s going to drive returns in the hedge fund industry?”

The story is a little different in Asia, however. Hedge fund managers in Hong Kong, speaking at an AIMA event on May 14, cut a bullish figure amid the somber conclusions written in London.

…Asian glory

Seth Fischer, chief investment officer and founder of Oasis Capital, a multi-strategy, market-neutral firm in Hong Kong, said: “The top of the pyramid [i.e. classical alpha-seeking managers] exists because it goes places were the machines can’t learn…

“Computers beat humans at Go because the computers were trained on lots of Go games. But [our firm] does things that are complicated, new, without precedent.”

George Long, founder and chief investment officer at LIM Advisors, another multi-strat in Hong Kong, says the proliferation of machine-driven strategies is only creating new inefficiencies elsewhere. As large, institutional capital seeks the kind of low-cost, scalable strategies driven by machines, they end up in one-way direction bets, he says.

“Alpha is still there for boutiques and specialists,” Long said, “because there are new inefficiencies in things that can’t be attacked by artificial intelligence.”

This is particularly true in Asia. Frontier markets such as Vietnam and Myanmar have little or no data for machines to parse. Big, liquid markets such as China throw up capital controls and market-access frictions. Japan is the sweet spot for classical hedge funds. It’s developed, liquid, and open for business – but it’s also opaque, and going through a cultural opening that is making room for activist investors.

“You can put a screen on corporate-governance decisions in Japan,” Fischer said. “But only two or three people really make the decisions. Google can predict what one million people think, but it has no idea what just three people think.”

In theory that could change as machines become more supple, the artificial intelligence more creative. But, says Julien Lepine, a specialist in multi-asset investments at Standard Aberdeen Investments, deep learning requires far more data than presently exists: “Today funds are only using machine learning in the simplest way.”

And looking further out, Fischer says the prestige of working at Amazon or Google will lose its edge. “They’re going to become more compliant, more like funds, and they’ll be less fun to work at,” he said.