Bank of England says it seeks industry feedback to the possibility of its creating a central-bank digital currency (CBDC).

In a webinar on April 7 led by Tom Mutton, director of fintech at the BoE, and his team laid out some of the biggest questions they face.

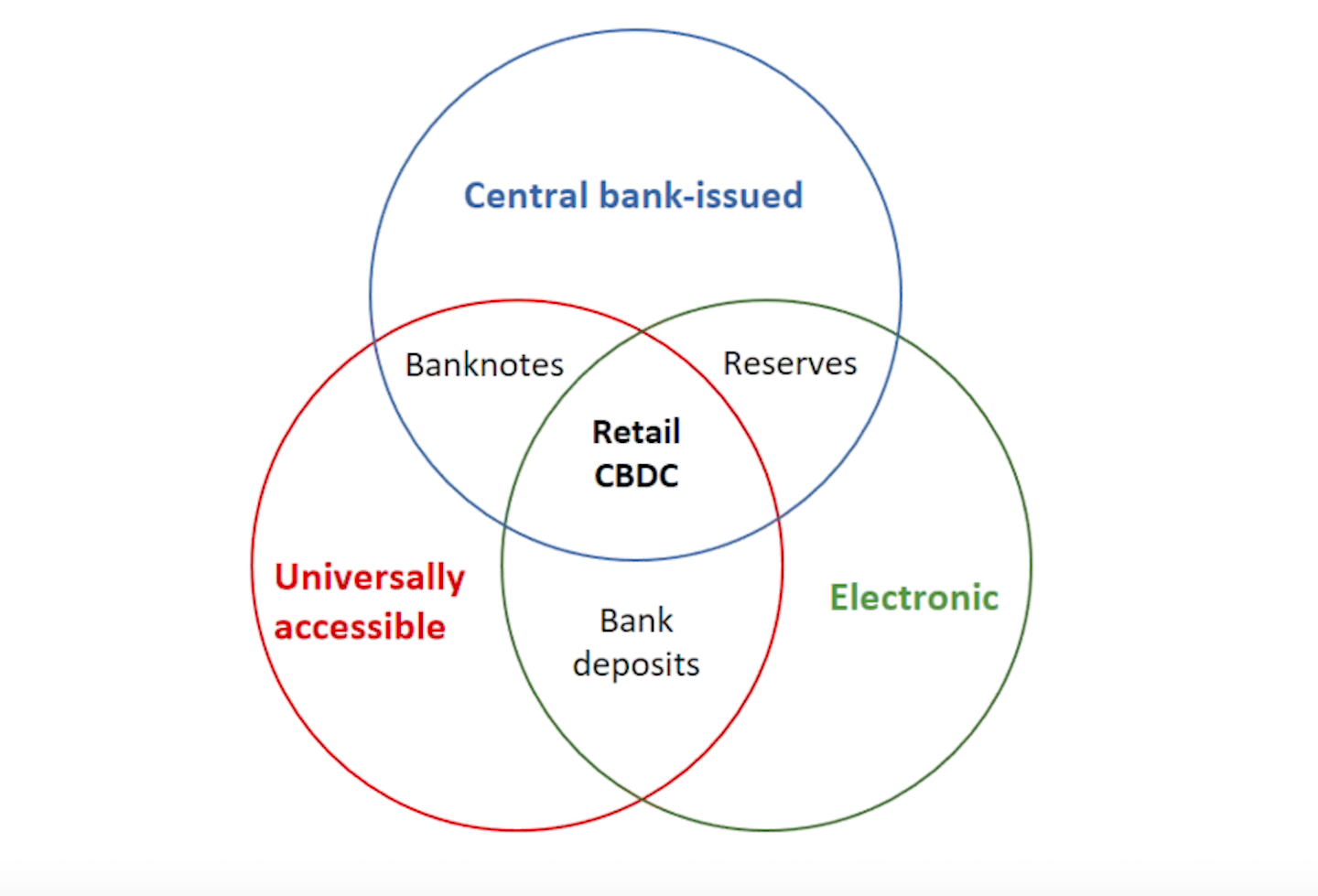

It defines a CBDC as an electronic form of money issued by BoE to be used by businesses and households as a store of value and a means of payment. Why issue one? To enable households and businesses to make fast, efficient, and reliable payments, while benefiting from an inclusive, innovative, competitive, and resilient payments system.

That implies tradeoffs in how it is designed, however, and a need for any CBDC to be widely adopted by the public.

The central bank doesn’t see cash disappearing, but it realizes that cash usage is now in decline, a trend now hastened by Covid-19 and the desire by many people to avoid handling coins and banknotes.

Roles and responsibilities

The first question BoE is asking the wider industry regards the balance of responsibilities and roles between the central bank and the private sector. The Bank’s team is leaning toward a hybrid model, which also was by far the most popular choice among the 1,200 people attending the webinar when asked by poll.

It is looking at a platform model in which the BoE provides a core ledger and processing technology, as well as sets standards and regulations, while commercial banks or other payments companies would interface with the public via APIs.

However, this still leaves plenty of design questions around what those standards and regulations should be, how private actors could access the service, and what services they make available to the public.

Technology

BoE executives say they the Bank’s requirements will dictate the technology, not the other way around. Getting the tech right will depend on what they want a CBDC to do, because there will be tradeoffs, such as between privacy and security, versus speed and efficiency.

The Bank’s fintech team has made clear it is unlikely to underpin a CBDC with distributed-ledger technology, and that they don’t expect a digital pound to resemble a cryptocurrency like Bitcoin.

Bank execs do not believe Bitcoin and its variants is a real form of money, as it fails on numerous counts – but they acknowledge that better technologies may emerge, including stablecoins. (The BoE team referenced unnamed proposals that sounded a lot like Facebook’s Libra.)

These emerging ideas might provide benefits that complement the existing payments system or meet future needs that don’t exist today. Stablecoins that operate at scale as a mainstream payment mechanism will need to come under the same standards, rules and safeguards as commercial bank money or BoE-issued banknotes.

There are therefore aspects of blockchain-based tech that the Bank may adopt. One is decentralization, which could enhance the system’s resiliency and make it easier to make a CBDC widely available – but decentralization can also slow performance and raises its own questions of privacy and security.

Privacy

A CBDC is often compared to cash, which is anonymous, but BoE executives said any electronic money must comply with regulations around money laundering and illicit activities. Therefore no CBDC can be as anonymous as cash. On the other hand, for a CBDC to achieve adoption means people must be confident that their payments activity remains private.

Some thorny questions loom around what data should be shared and who can see it. This is further complicated because the BoE is not a privacy body. Its job is to ensure monetary and financial stability. It will need to consult with government and politicians on such questions.

Programmable money

Another potential advantage to DLT is smart contracts and making money programmable. This could allow innovations such as micropayments, which are not feasible in today’s world. DLT could also bring benefits in cryptography and the sharing of data while protecting privacy.

One-third of the webinar audience thought programmability was the most useful feature that DLT could enable.

BoE executives noted that they have studied DLT for several years and so far have found it insufficient to perform as well as the existing payments infrastructure, or possess the capacity to handle the volumes in BoE’s real-time gross settlement system. The tech isn’t ready to serve as a piece of critical infrastructure. But BoE is in the midst of upgrading its RTGS system so that it can plut into future blockchain-based systems.

Benefits and risks

A third area in which BoE is keen to solicit industry feedback concerns public demand for a CBDC: a digital pound only makes sense if people use it. This implies a shift away from commercial bank deposits, which BoE reckons is inevitable, but it doesn’t want to see a dramatic swing that would destabilize commercial banks.

Commercial banks could suffer from costlier funding needs, which would impact the quality and volume of lending and credit creation, which in turn would hurt the economy. The CBDC’s design must accrue benefits with minimum negative impact.

This leads to questions of whether, and to what degree, the CBDC is built to attract demand versus other forms of money or bank deposits. Should the BoE impose restrictions on who can hold digital pounds, who can transfer it, how much can be held or transferred, what other forms of money can it convert in and out of, and – most intriguingly – should digital pounds pay interest?

The webinar audience felt that questions of convertibility and access to CBDCs were the most important factor, with each garnering about one-third of a poll vote; another 25% said remuneration was the most important factor. Relatively few people thought restrictions on holding or transferring CBDC would drive adoption.

The BoE team raised other questions, including a CBDC’s use in government activities such as taxation; its energy requirements; cyber-security; and whether a CBDC should also be used at the wholesale level.

They welcome views from the industry, which can be sent to them at [email protected].